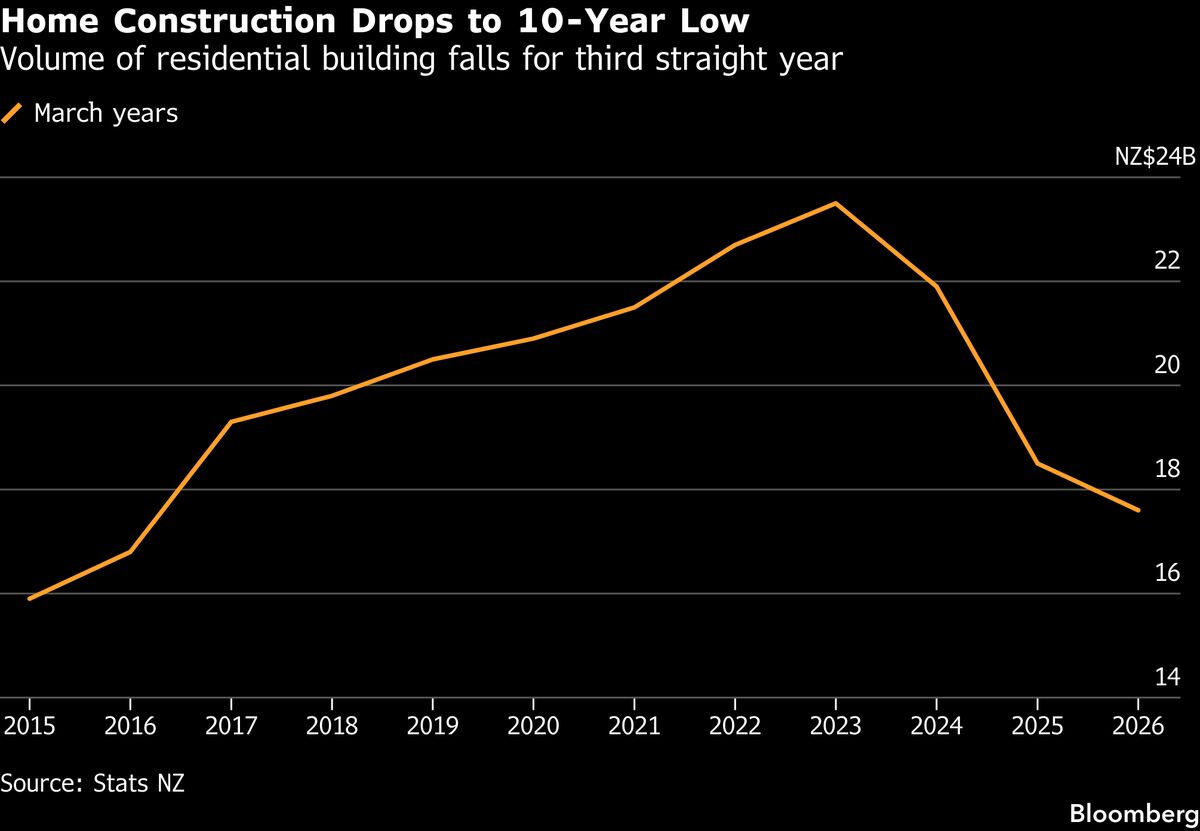

Key facts

- UK house prices fell for the third consecutive month in May.

- UK home price growth forecast for the year revised down to 1.8%.

- London property market expected to see a 0.3% price decrease this year.

- UK mortgage approvals for house purchases reached their highest level in over a year.

- US housing market list prices dropped significantly in May.

- US new housing listings surged in the Northeast and Midwest in May.

- US housing recovery paused as sales and new listings declined in May compared to last year.

- US mortgage rates rose above 6.5%.

- HELOC and home equity loan rates increased on June 5, 2026.

- Australian home prices are projected to grow by 1.0% this year, the slowest since 2022.

- Greater Toronto Area home sales increased 10% in May from April.

- Greater Toronto Area home price index dipped 0.2% month-over-month.

Global housing markets are navigating a complex environment characterized by rising interest rates, persistent inflation, and geopolitical uncertainties, leading to varied outcomes across regions. In the United Kingdom, house prices have fallen for three consecutive months, with May marking the latest decline. The annual forecast for UK house price growth has been revised downward to 1.8% for the year, a decrease from the previous 2.5% projection, largely attributed to elevated borrowing costs and inflation dampening buyer demand. London's property market is specifically expected to see a 0.3% price decrease this year. Despite these price trends, UK mortgage approvals for house purchases reached their highest level in over a year in May, suggesting increased market activity. However, economists caution that further interest rate hikes later in the year could impact borrowing costs.

The United States housing market presented a contrasting scenario in May, with list prices experiencing significant drops while buyer activity saw an increase. New listings surged in the Northeast and Midwest regions, reversing earlier declines. Despite this uptick in activity, the broader housing recovery appears to be paused, as indicated by a decline in sales and new listings compared to the previous year, with mortgage rates rising above 6.5%. Home equity line of credit (HELOC) and home equity loan rates also increased on June 5, 2026, coinciding with falling asking prices for homes, signaling a notable shift towards higher borrowing costs and lower property values.

Australia's housing market is projected to experience its weakest growth since 2022, with median home prices expected to increase by only 1.0% this year. This slowdown is attributed to higher mortgage rates and cost-of-living pressures, which are significantly affecting affordability and demand, particularly for first-time buyers. In Canada, the Greater Toronto Area saw a 10% increase in home sales in May compared to April, representing the largest monthly gain in ten months. However, the home price index in the region dipped by 0.2% month-over-month, settling at C$927,800. This market dynamic in Toronto is partly explained by improved affordability resulting from lower prices and borrowing costs.

These housing market trends are occurring against a backdrop of shifting global monetary policy expectations. Middle East tensions and ongoing inflation concerns are influencing rate hike expectations. The European Central Bank (ECB) and the Bank of Japan (BoJ) are anticipated to raise rates in June. In contrast, the US Federal Reserve (Fed) saw a slight upward shift in rate hike expectations, while the Reserve Bank of New Zealand (RBNZ) has a high probability of a hike. The Bank of England (BoE), Reserve Bank of Australia (RBA), Bank of Canada (BoC), and the Swiss National Bank (SNB) are generally expected to hold their current rates.